1. What is the Active Grille Shutter Market Overview – definition, scope, and significance?

The Active Grille Shutter (AGS) market comprises suppliers of aerodynamic devices mounted on the front fascia of vehicles that open or close automatically to regulate airflow. These shutters improve fuel efficiency, reduce emissions, and enhance cooling performance across passenger cars, light commercial vehicles, and heavy commercial vehicles. The market’s scope covers hardware (horizontal and vertical vane types), propulsion systems (internal combustion engine‑driven and electric), and related software controls, making it a strategic component in modern vehicle design and sustainability goals.

2. What are the Active Grille Shutter Market Drivers, Restraints, Challenges, and Opportunities?

Key drivers include tightening fuel‑economy regulations, growing consumer demand for greener vehicles, and OEMs seeking cost‑effective aerodynamic solutions. Restraints stem from the added complexity of integrating shutters into existing vehicle architectures and higher upfront component costs. Challenges involve ensuring reliability under extreme temperature cycles and meeting diverse regional safety standards. Opportunities arise from electrification trends that favor lightweight electric‑actuated shutters, and from aftermarket retrofits for commercial fleets seeking operational savings.

3. What are the current Growth Trends in the Active Grille Shutter Market?

Current trends show a shift toward electric actuation, driven by higher precision and lower emissions compared with internal‑combustion‑engine mechanisms. Horizontal vane designs are gaining popularity for their compact packaging, while vertical vanes remain strong in heavy‑duty applications. OEMs are increasingly embedding AGS control algorithms within vehicle ECU software, enabling dynamic adaptation to driving conditions. Collaborative development projects between tier‑1 suppliers and automakers are accelerating technology standardization.

4. How has COVID‑19 impacted the Active Grille Shutter Market and what is the recovery trajectory?

The pandemic caused a temporary dip in production volumes due to plant shutdowns and supply‑chain disruptions. However, the market rebounded quickly as recovery in passenger‑vehicle sales accelerated and commercial‑vehicle demand resumed. Post‑COVID, manufacturers have prioritized efficiency upgrades, reinforcing the relevance of AGS solutions. The recovery trajectory is positive, with a clear path toward sustained growth as manufacturers integrate AGS to meet future efficiency mandates.

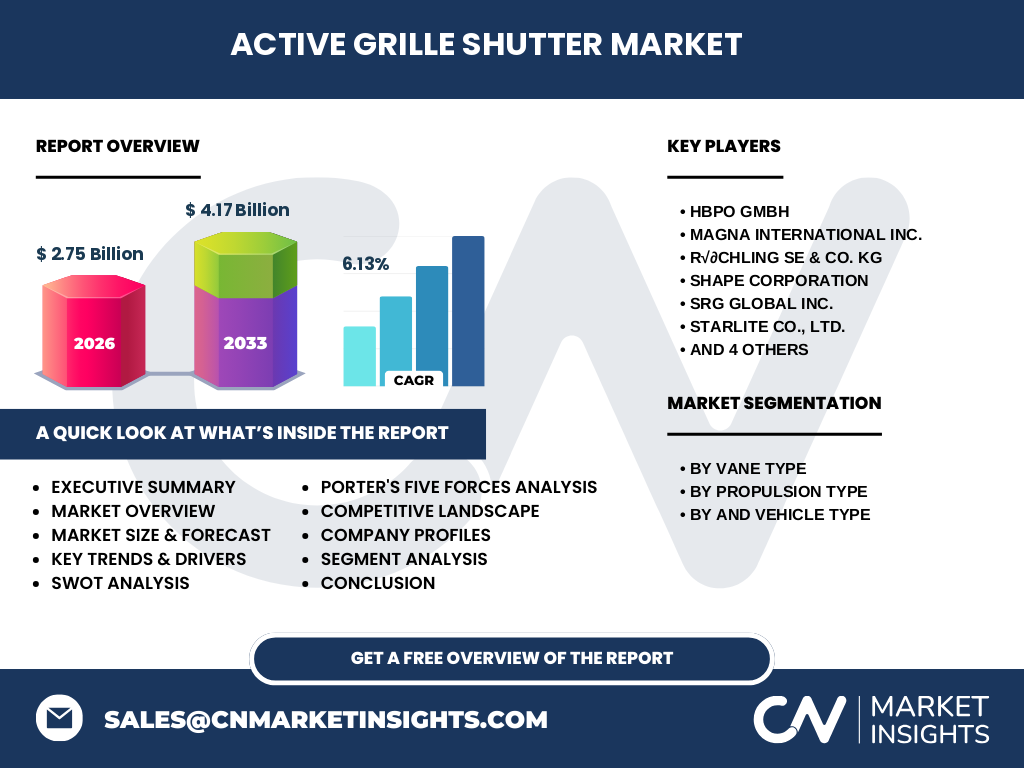

5. Who are the major competitors in the Active Grille Shutter Market and what is the level of consolidation?

Leading competitors include HBPO GmbH, Magna International Inc., R√∂chling SE & Co. KG, SHAPE Corporation, SRG Global Inc., STARLITE Co., Ltd., Standard Motor Products Inc., Techniplas, LLC, Valeo SA, and Wirthwein AG. The market exhibits moderate consolidation, with a handful of tier‑1 suppliers commanding significant OEM contracts while a broader base of specialized firms focuses on niche vane designs or propulsion technologies. Strategic partnerships and joint ventures are common as firms aim to broaden product portfolios.

6. What are the key findings in the Executive Summary of the Active Grille Shutter Market?

The market is valued at $2.75 billion in 2026 and is projected to reach $4.17 billion by 2033, delivering a CAGR of 6.13 %. Growth is propelled by regulatory pressure, electrification, and the expanding commercial‑vehicle segment. Horizontal vanes and electric actuation are the fastest‑growing segments. The competitive landscape is dominated by a mix of established tier‑1 suppliers and innovative niche players, creating a dynamic environment for strategic investments.

7. What is the forecast for the Active Grille Shutter Market from 2025 to 2032?

Based on the provided CAGR of 6.13 %, the market is expected to maintain steady expansion through 2032, surpassing the $4 billion mark by the early 2030s. Demand will be driven by increasing adoption in electric‑vehicle platforms, regulatory incentives for aerodynamic efficiency, and growing retrofit activity in commercial fleets seeking operational cost reductions.

8. How is the Active Grille Shutter Market sized and shared by segment?

Segmentation is organized by vane type (horizontal, vertical), propulsion type (internal combustion engine, electric), and vehicle type (passenger, light commercial, heavy commercial). Horizontal vanes command a larger share in passenger‑vehicle applications due to packaging advantages, while vertical vanes remain prevalent in heavy commercial vehicles where robust cooling is critical. Electric propulsion is gaining share rapidly, especially in newer passenger‑car platforms, whereas internal‑combustion actuation continues to dominate legacy fleets.

9. What is the Global Active Grille Shutter Market size and share by region?

While specific regional monetary values are not disclosed, the market’s global footprint spans North America, Europe, Asia‑Pacific, and the rest of the world. Developed regions such as Europe and North America lead in early adoption due to strict emissions standards, while Asia‑Pacific shows the highest growth potential driven by expanding automotive production volumes and increasing regulatory focus on fuel efficiency.

10. What does the Regional Analysis reveal about the Active Grille Shutter Market?

Europe demonstrates strong OEM demand for AGS in premium passenger cars, supported by stringent EU CO₂ targets. North America’s growth is linked to commercial‑vehicle fleet electrification and a focus on after‑market upgrades. Asia‑Pacific’s rapid industrialization and large manufacturing base make it a hotspot for both original equipment integration and cost‑effective aftermarket solutions. Emerging markets in Latin America and the Middle East are beginning to explore AGS as part of broader efficiency programs.

11. Which companies lead the Active Grille Shutter Market and what are their strategies?

Key leaders such as Valeo SA and Magna International Inc. focus on electric‑actuated solutions and advanced software integration. HBPO GmbH leverages its extensive body‑in‑white expertise to embed AGS early in vehicle development. R√∂chling SE & Co. KG emphasizes modular designs for easy retrofit. Companies like STARLITE and SRG Global pursue strategic acquisitions to broaden their product portfolios, while Techniplas, LLC and Standard Motor Products Inc. target niche commercial‑vehicle segments.

12. How does Porter’s Five Forces analysis apply to the Active Grille Shutter Market?

Threat of new entrants is moderate; high R&D costs and OEM validation create barriers. Bargaining power of suppliers is low to moderate, as many component suppliers exist. Bargaining power of buyers (OEMs) is high, given their scale and the importance of performance specifications. Threat of substitutes remains limited; alternative aerodynamic solutions exist but lack the dynamic control of AGS. Industry rivalry is intense, driven by technology differentiation and cost‑competitiveness.

13. What are the SWOT findings for the Active Grille Shutter Market?

Strengths: Proven fuel‑efficiency benefits, alignment with regulatory trends, and expanding applicability across vehicle classes.

Weaknesses: Integration complexity and higher upfront costs.

Opportunities: Electric actuation, aftermarket retrofits, and growth in emerging markets.

Threats: Potential competition from alternative aerodynamic technologies and tightening cost constraints in budget vehicle segments.

14. How is the value chain structured for the Active Grille Shutter market?

The value chain begins with raw material suppliers (aluminum, high‑strength steel, composites), proceeds to component manufacturers that produce vane assemblies and actuation mechanisms, followed by system integrators that embed AGS into vehicle platforms. Software developers provide control algorithms, while OEMs act as the final assemblers. After‑market service providers and distributors complete the chain by offering maintenance, retrofit kits, and spare parts.

15. What key investment insights can be drawn for the Active Grille Shutter Market?

Investors should target companies with strong electric‑actuation portfolios and robust OEM relationships, as these are positioned to capture the fastest‑growing segments. Partnerships that combine hardware expertise with software control capabilities are especially attractive. Additionally, firms focusing on aftermarket solutions for commercial fleets present upside potential, given the cost‑saving incentives driving retrofits.

16. What are the concluding takeaways from the Active Grille Shutter Market analysis?

The AGS market is on a clear growth trajectory, underpinned by regulatory demands and the shift toward electrification. Horizontal vanes and electric propulsion dominate emerging demand, while vertical vanes retain importance in heavy‑duty contexts. Competitive dynamics favor firms that can deliver integrated, software‑enabled solutions. The forecasted CAGR of 6.13 % signals a robust investment case for stakeholders willing to navigate integration challenges.

17. How was the research for this report conducted?

The study combined primary interviews with OEM engineering teams and tier‑1 suppliers, secondary analysis of industry publications, regulatory filings, and financial statements of listed players. Market sizing leveraged the provided 2026 baseline of $2.75 billion and applied the stated CAGR of 6.13 % to project forward values. Segmentation was mapped using the defined vane, propulsion, and vehicle-type categories.

18. What is the scope of this research and its limitations?

The scope covers global AGS demand across passenger, light commercial, and heavy commercial vehicles, segmented by vane and propulsion types. Geographic coverage includes major automotive regions, but specific regional revenue figures are not disclosed. The analysis does not extend to detailed cost‑structure breakdowns or proprietary OEM design data, focusing instead on market‑level trends and competitive positioning.

19. Which key companies have recent developments in the Active Grille Shutter market?

Valeo SA announced a new electric‑actuated AGS line optimized for next‑generation electric sedans. Magna International Inc. unveiled a collaborative project with a leading European OEM to integrate horizontal shutters into a high‑efficiency SUV platform. HBPO GmbH launched a modular retrofit kit for light commercial vehicles, enabling fleet operators to upgrade existing trucks with minimal downtime. SRG Global Inc. completed an acquisition of a niche vertical‑vane specialist, expanding its heavy‑duty portfolio.